")

")

Dividing by Four the CO2 Emissions from France in the Energy Sector: the Negatoe Scenario 2017

- Published on 26 February 2018

Dividing by Four the CO2 Emissions from France in the Energy Sector: the Negatoe Scenario 2017

Save the Climate by the Scenario Committee

Claude Acket, Hubert Flocard, Claude Jeandron, Hervé Nifenecker,

Henri Prévot, Jean Marie Seiler

Table of Contents

Foreword.............................................................................................................................................. 2

Introduction to Negatoe 2017.............................................................................................................. 6

- A) The Starting Point for France, the Situation in 2015...................................................................... 8

A 1) Primary Energy Supply per Resource for year 2015................................................................ 9

A 2) 2015 Final Energy Consumption per Usage in Mtoe............................................................... 9

A 3) Specific Point on Electricity in 2015 (TWh).......................................................................... 10

A 4) Specific Point on Renewable Energies in 2015..................................................................... 11

A 5) Carbon dioxide emissions in 2015 (energy sector)................................................................ 11

B ) The Negatoe Approach: Beyond the Accomplished Coal Phase-Out ......................................... 12

C ) An Outlook on the Future ........................................................................................................... 13

- D) Energy Demand Management: 2050 Target.................................................................................. 16

D.1 General Considerations........................................................................................................... 16

D 2: Residential Sector.................................................................................................................. 18

D 2.1: Heating........................................................................................................................... 19

D 2.2: Domestic Hot Water...................................................................................................... 23

D 2.3. Cooking.......................................................................................................................... 24

D 2.4. Specific Electricity Uses................................................................................................ 24

D 3. Tertiary Sector........................................................................................................................ 25

D 4. Industrial and Agricultural Sectors........................................................................................ 25

D 5 Transportation......................................................................................................................... 26

D 5.1. Initial Conditions and Trend.......................................................................................... 27

D 5.2 Future: Sobriety and Efficiency .................................................................................... 27

D 5.3. Replacing Oil: Biofuels and Electricity......................................................................... 28

D 5.4. Transportation Recap..................................................................................................... 30

D 6 Global Recap: Final Energy Demand..................................................................................... 30

- E) Carbon Free Energy Sources from Now to 2050.......................................................................... 31

E 1. Renewable Direct Heat Sources............................................................................................. 31

E 1.1. Biomass, Biogas, Carbonaceous Wastes ........................................................................ 31

E 1.2. Miscellaneous Heat Renewables Other than Biomass.................................................... 33

E 2: Direct Electricity Renewables................................................................................................ 33

E 2.1 Hydropower.................................................................................................................... 34

E 2.2 Wind Power..................................................................................................................... 35

E 2.3 Photovoltaic..................................................................................................................... 39

E 2.4 Various wastes, wood, .................................................................................................... 40

E 2.5 Overall Assessment of Electric Power Renewables........................................................ 40

E 2.6 What Should We Make of Decentralized Energy Systems?........................................... 41

E 3. Nuclear Power........................................................................................................................ 41

- F) Final Negatoe Wind Up................................................................................................................. 44

F 1. The Objective: Minimal Cost ................................................................................................ 44

F 2. A Gradual Approach to Achieve the Factor 4....................................................................... 45

F 3. Main Results of the Negatoe Wind Up.................................................................................. 46

F 3.1. Final Energy.................................................................................................................... 46

F 3.2. Electricity........................................................................................................................ 47

F 3.3: Supply, Primary Energy Resources, 2015-2050 Transition............................................. 49

F 3.4: Fossil Fuels and Carbon Dioxide Emissions....................................................................... 49

- G) The Financial Aspects: the Cost of the Energy Transition............................................................ 50

- H) Discussion..................................................................................................................................... 52

Acronyms........................................................................................................................................... 53

References.......................................................................................................................................... 55

Appendix 1: Electricity and Grid Balance......................................................................................... 56

Appendix 2: Electricity and Hydrogen.............................................................................................. 62

Appendix 3: Methane Production Modes.......................................................................................... 64

Appendix 4: Principal Economic Evaluation Hypotheses ................................................................. 66

Appendix 5: An Economic Comparison at the European Scale......................................................... 67

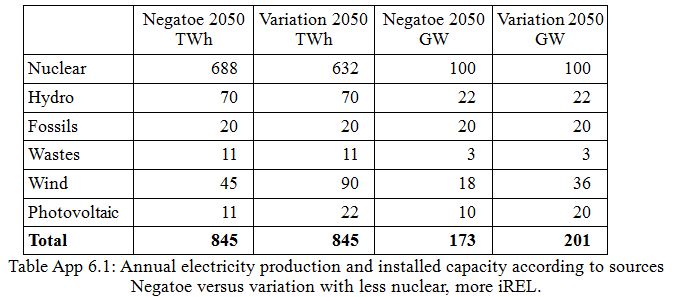

Appendix 6: Negatoe Variation: Towards Less Nuclear Power 69

Foreword

From Negatoe 2007 to Negatoe 2011, Negatoe 2014 and the 2015 energy transition law (loi de transition énergétique de 2015)

The 2005 energy transition legislation defined four main objectives for the French energy policy; these objectives remain current:

- Contribute to the national independence for energy and guarantee the security of supply.

- Ensure a competitive energy price.

- Protect the environment, in particular by mitigating greenhouse gas emissions

- Guarantee social and territorial cohesion by ensuring an access to energy for all.

In the frame of this legislation, France supports the international goal of dividing global greenhouse gas emissions by two by 2050[1], which requires a division by a factor[2] 4 to 10 of the emissions due to developed countries.

The 2005 legislation defines four major orientations for attempting to reach the objectives:

- Save energy.

- Decarbonate the energy consumed by reducing the fossil energy share.

- Develop renewable energy sources

- Continue with nuclear energy for electricity generation

At the national debate on energy of 2003 (débat national sur les énergies - DNE 2003) organized in preparation for the policy guideline law of 2005, we presented, under the name "fossil phase-out", what became, in 2007, a scenario based on the 2006 data that we subsequently renamed Negatoe. This scenario is consistent with the goals of the legislation and allows reaching the "factor 4". As it is, it applies to the situation in France but it could be adapted to the conditions of most developed countries.

This scenario is along the lines of the first energy transition operated by France in the years 1980-1990, during which nuclear energy replaced coal and oil in electricity generation, a first significant step towards energy decarbonation.

We called it "Negatoe" because, indeed, it is the consumption of energy produced in large part by fossil fuels, symbolized by oil and the tonne of oil equivalent (toe) that has to be managed[3]. Beyond energy conservation, without which the "factor 4" would not be attainable, fossil fuels must be replaced wherever possible by carbon free energies, whether for direct use, to produce heat, or to generate electricity.

In its Negatoe 2011 version, this scenario was presented by Save the Climate at the National Debate on the Energy Transition (DNTE - Débat National sur la Transition Energétique) that was held from November 2012 to mid 2013. Negatoe was placed in the DEC category and was one of the four trajectories retained in the debate overview.

- In the SOB family (SOB for sobriety), the Negawatt scenario with its total nuclear phase-out implies a 60 % reduction of per capita final energy consumption all sources taken together, and anticipates a 272 TWh final electricity consumption (compared to 432 TWh in 2015, i.e. a 43% per capita reduction in the electricity sector).

- In the EFF family (EFF for efficiency), the ADEME[4] scenario assumes a 51 % reduction of per capita final energy consumption for a total electricity generation of 381 TWh of which 265 TWh from renewables, 95 TWh from nuclear[5] and 21 TWh from natural gas.

- In the DIV family (DIV for diversified), the ANCREdiv[6] scenario anticipates a 17 % reduction of per capita final energy consumption. This scenario conforms to the government directive to reduce the share of nuclear energy to 50 % and reaches 250 TWh nuclear generation (in a total 510 TWh electricity generation).

- The DEC family (DEC for decarbonated via electricity) includes the ANCREele scenario and the scenario called Negatoe. The ANCREele scenario differs from the ANCREdiv scenario in that it maintains the contribution of nuclear power to about its present level, with a 750 TWh total electricity generation of which 420 TWh is nuclear (approximately today's value) and 316 TWh from renewables. As for Negatoe, it puts even more emphasis on decarbonated electricity, partly replacing gas for heating and oil for mobility. It disputes that, because of intermittence and variability, renewables will be able to take a predominant share in electricity generation. At the time, the scenario planned 908 TWh electricity[7] (+61% compared to the 2012 value), with 700 TWh nuclear (+64%) and 168 TWh renewables (+92%). Overall, the nuclear generation share is about the same as today's (77%) but its absolute value is increased. However, in terms of installed power, nuclear power accounts for a little less than half the total.

The National Debate on the Energy Transition allowed a comparison of different scenarios that all planned a division by 4 of the CO2 emissions, based on a more or less intense reduction of energy needs, on a combination of sobriety and efficiency, on the future of renewable energies and, more than anything else, because it is structuring, on the share of nuclear power in electricity generation, extending from complete nuclear phase-out (Negawatt case), through very little nuclear - actually equivalent to none (ADEME case), on to a little less or as much as today (ANCRE cases), to finally, with no preconception, increased nuclear power, as necessary in order to satisfy needs at lowest cost (Negatoe case).

During the debate, the French government gave clear indications concerning its preconceptions and orientations, leading to significantly reduced nuclear power. This was officially confirmed with the legislation: "Loi sur la transition énergétique pour la croissance verte" (Law on the energy transition and green development) approved and passed by parliament in July 2014, published in the Journal Officiel (official journal) in August 2015.

This law refers clearly to the fundamental goal discussed at the beginning of this chapter : 40% reduction of greenhouse gas emissions between 1990 and 2030 and division by 4 of greenhouse gas emissions between 1990 and 2050 and, quite consistently, stipulates that the fossil fuel generated primary energy consumption must be reduced by 30% in 2030 relative to the 2012 reference. We note the explicit qualifier fossil fuel.

But this law, by sometimes confusing the goals reaffirmed above and some of the means to reach them, goes beyond and engages specific actions. Such means are not all directly related to the fundamental goal of reducing carbon dioxide emissions and can, without being detrimental to the goal, not concern it directly or, even, be counterproductive. Thus, it puts forward, for instance:

- a 50% reduction of final energy consumption in 2050 relative to the 2012 reference, with a 20% intermediate goal in 2030.

- an increased renewable energy share, accounting for up to 23% of the gross final energy consumption in 2020 and 32% of this consumption in 2030.

Concerning the first item above, if reducing energy consumption is, indeed, essential if the factor 4 is to be reached, yet, within which limits and at what cost this reduction needs to be done should also be stated. Consumption reduction can be achieved at the expense of other more effective actions towards the reduction of emissions; conserving energy can turn out to be very expensive, in contradiction with the popular saying that energy that is not produced costs nothing. Conserving energy is not typically related to the principal goal, that of reducing carbon dioxide emissions. A significant emissions reduction can quite well be obtained with constant final energy consumption. Moreover, considering the connection between economic growth and energy consumption, barring considerable energy intensity advances, too large a reduction of the energy consumption can translate into economic decline synonymous with poverty and unemployment.

Concerning the second item, although there is total agreement for the development of renewables in general, yet it is necessary to be more specific. If this support need not be dubious, except for cost and, possibly, land use issues where thermal renewables (including biomass and solar generated domestic hot water ...) are concerned, it becomes debatable where electric power generating renewables are concerned such as wind power and photovoltaics, because of their costs but more so because of their variability and their intermittency. They require backup systems which, in the absence of acceptably efficient and inexpensive storage devices, lead to boosting natural gas power generators, thus defeating carbon dioxide emissions reduction.

It seems, though, that the real goal of this law is revealed through the actions aimed directly at nuclear power, thus catering to electoral objectives:

- reduce to 50% the share of nuclear power in the production of electricity by 2025.

- limit the total nuclear electricity production capacity to 63.2 GWe (note that this is the current capacity, before the new EPR type reactor being built in Flamanville 3 becomes operational).

Yet, if the decarbonation goal of our economy is to be reached, the large amounts of fossil energy consumed in transportation and buildings will have to be replaced progressively with carbon free electricity.

We have carefully examined the various means available to produce carbon free electricity while taking into account the stringent technical constraints that have to be complied with if a reliable and good quality electricity is to be provided. Because the intermittency of wind and photovoltaic power has to be overcome, the low cost power fleets allocate a large share to nuclear production and will continue to do so. That is how electric power generation will best preserve consumer purchasing power and will provide industry with a competitive edge relative to foreign competition.

This is why, in keeping with previous work, we propose this 2017 update of the so-called Negatoe scenario. It does not conform to the 2015 legislation where the specific nuclear issue is concerned but it has its full place in the debate, in that it brings it back to the primary objective: reducing carbon dioxide emissions by a factor 4.

Introduction to Negatoe 2017

Negatoe directly addresses the four main energy policy goals which are more than ever on the agenda.

- Contribute to national independence for energy and guarantee security of supply.

- Ensure a competitive energy price.

- Protect the environment, in particular by mitigating greenhouse gas emissions, this being put forward strongly at the Paris COP21[8].

- Guarantee social and territorial cohesion by ensuring an access to energy for all.

Negatoe defines four major lines of action to help reach the goals specified:

- Energy conservation. Moderation, encouraged and made acceptable to all but within limits excluding coercion and, more important, Efficiency which generally requires large investments but these should have a reasonable payback period.

- "Decarbonate" the energy consumed by reducing the share of fossil energies[9], in order to achieve the factor 4 division by 2050, then proceed further to reach zero emissions by the end of the century. Nuclear power has replaced coal[10] and heavy oil in the 1980s-1990s for electricity generation in France. The task remains, now, to replace oil and natural gas in all their other uses.

- Develop renewable energies, distinguishing thermal from electricity generating renewables.

- Keep nuclear power for the generation of electricity without a priori excluding its extension along the lines of what was achieved during the first true energy transition of the 1980s and 1990s that witnessed the end of coal and heavy oil in the French electricity mix.

In the first chapter (A), we present the energy situation as it stands in 2015 and discuss the estimation of carbon dioxide emissions related to the energy sector in France, viz. 344 million tonnes.

In the second chapter (B), we show that France has already traveled a long way towards reducing its carbon dioxide emissions with the development of nuclear power in the years 1980-1990, and the quasi total phase-out of coal and heavy oil. This achievement deserves to be analyzed and its lessons learned so as to proceed further and now reduce natural gas and oil consumption.

In the third chapter (C), we discuss a so-called reference scenario, one which could be implemented in semi continuity with the present, were it not for the imperative division by 4 of fossil fuel use.

In the fourth chapter (D), we deal with demand management in the 2050s. We discuss the moderation issues (individual and collective endeavors towards demand reduction) and the efficiency measures liable to reduce carbon dioxide emissions for a given demand.

In the fifth chapter (E), we review the potential of the different carbon free energy sources (renewables and nuclear) in satisfying the demand with no carbon dioxide emissions.

In the sixth chapter (F), we recapitulate the main Negatoe scenario data for 2050, along with the state of the final energy demand for each energy source; we examine electricity with special attention and assess the carbon dioxide situation.

In the seventh chapter (G), we estimate the cost of the Negatoe energy transition via a simplified economic approach.

Preliminary Remarks:

- 1. Energy occurs in many forms (heat, mechanical energy, electricity). It is measured with a standard unit regardless of its form, i.e. the Joule and its multiples (MJ, GJ[11], ..). In practice, however, professionals, because of the leading role played by oil, have adopted the toe, for tonne of oil equivalent, as their reference unit, along with its multiples (toe, Mtoe, Gtoe) for all thermal energies, and the kWh and its multiples (MWh, GWh, TWh) for electricity:

1 toe = 41.86 GJ (often rounded off to 42 GJ)

1 MWh = 3.6 MJ or 0.086 toe

Although electricity and heat do not serve the same purposes, the international and national organizations that deal with energy have agreed to express in toe the energy made available to its users, called "final energy", whether the energy is thermal or electric. We generally adopt this convention here, given that our purpose is to examine the evolution of consumption and of the means to satisfy the demand. Per capita or per household consumption, however, will often be expressed in kWh, a more convenient unit in these instances.

From Final Energy to Useful Energy

Final energy is, according to convention, the energy made available to the user for a price.

By summing her/his bills for electricity, gas, oil (for heating) or gasoline (for the car), etc a consumer can calculate his/her final energy expenses in financial but also in energy terms, i.e. how much final energy is consumed. This final energy fulfills the energy needs in that it provides the useful energy, i.e. the energy that remains once the losses are subtracted; for example, a gasoline combustion engine's efficiency can be as low as 30 %. Thus, only 30 % of the so-called final energy really moves the vehicle. On the other hand, an electric engine on the same vehicle has an efficiency that can reach 90 % so that the final energy will be enough to travel three times as many miles. Indeed, useful energy is the issue and with minimal carbon dioxide emissions.

Taking another approach, instead of considering losses, additional input can be taken into account, with pumped energy. Indeed, final electricity can be used by heat pumps to pump energy from nature that will come as an addition to the electricity. Again a particular advantage of electricity that is to be taken into account.

Conversely, in the assessment of CO2 emissions, quite obviously, the tonnes of fossil fuels that have effectively contributed to making the final energy tonnes available are the quantity that must be examined. The former are somewhat in excess of the latter where the final use is heat production (taking oil as an example, the energy consumed in refining and conveying the fuel to the end user represents 10 to 20 %) but, in the case of electricity, it is twice to 3.3 times as much (taking thermal efficiency into account in the conversion of heat to electricity[between 33 and 60 %], the losses on the grid, and the consumption of auxiliary production equipment).

Once these so-called "primary" energy amounts are evaluated, the pertaining CO2 emissions, or rather their carbon content expressed in terms of tonnes of carbon (tC and its multiples), can be assessed by applying the standard coefficients[12]:

- Oil: 1 toe yields 0.89 tC

- Coal: 1 toe yieds 1.17 tC

- Natural gas: 1 toe yields 0.74 tC

The conversion from tC to tCO2 is obtained by multiplying these values by 44/12=3.65

The conversion of 1 toe of fossil fuel generated electricity to tC (or tCO2) is obtained by dividing by the thermal efficiency of the production unit[13].

- 2. With this paper, we aim at an initial evaluation of the various factors that contribute to the "energy mix" and CO2 emissions[14].

A) The Starting Point for France, the Situation in 2015

As discussed above, the Negatoe 2007 and 2011 versions were based on the 2006 data. The onset of the recent financial crisis (early summer 2007) and the collapse of Lehman Brothers (in September 2008) whose effects are still with us, have totally disrupted the data, affecting both the GDP and the energy consumption in unforeseen ways. Indeed, while in 2007 the real Gross Domestic Product was growing at a rate of 2.3% per year, it was declining by 0.1% per year in 2008 and by 3.1% in 2009. These downturns were compensated with difficulty thanks to a return to growth: 1.7% in 2010, 2% in 2011, but only 0.2% in 2012 and 0.6% in 2013 and 2014 and, finally, 1.3% in 2015.

Concerning energy, the extent of the crisis can be measured in terms of final energy consumption which declined from 161.7 to 149.2 Mtoe in 2015 (-7.7%). This reduction does not result from voluntary energy management measures but reflects an economic decline leading to unemployment, loss of purchasing power and the associated social consequences.

Given this situation, a clear vision of what the future holds requires basing this Negatoe 2017 version on the 2015 data[15].

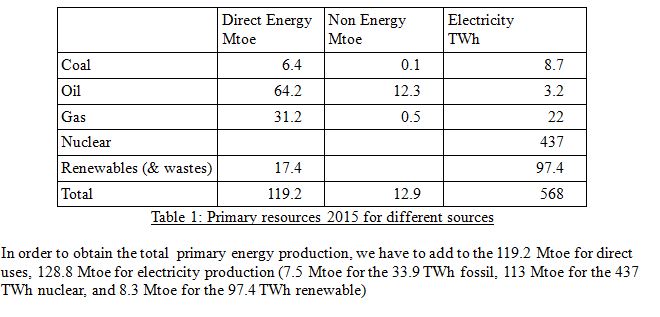

A 1) Primary Energy Supply[16] per Resource for year 2015

Table 1: Primary resources 2015 for different sources

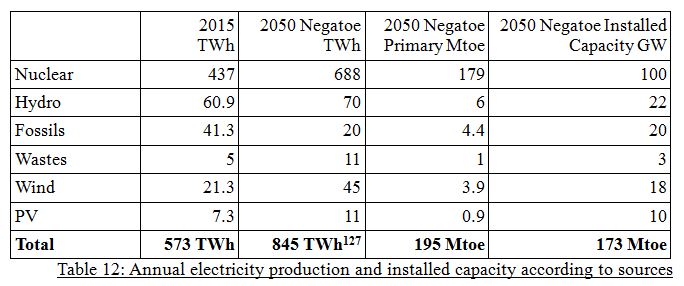

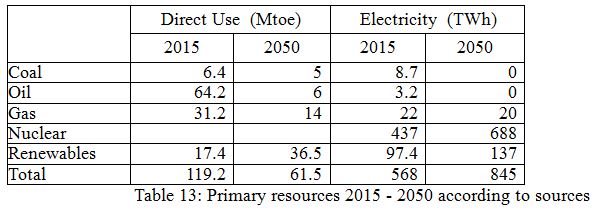

In order to obtain the total primary energy production, we have to add to the 119.2 Mtoe for direct uses, 128.8 Mtoe for electricity production (7.5 Mtoe for the 33.9 TWh fossil, 113 Mtoe for the 437 TWh nuclear, and 8.3 Mtoe for the 97.4 TWh renewable)

Fossil fuels account for 109.2 Mtoe in primary production. A factor 4 division would imply doing away with almost 90 Mtoe, either by reducing global needs by the same amount, all sources included, or by replacing them with carbon free sources, for direct heat production and electric power generation.

Note: In a global perspective, the summing of direct heat energy and electricity to obtain what is called primary energy measured at the production outlet, implies conventional conversions which, in France, are based officially on the energy content rule. The conversion defines the amount of reference fossil fuel (oil) that would be consumed to produce 1MWh. The values are 1MWhe of nuclear electricity is said equivalent to 0.26 toe, 1 MWhe of fossil fuel electricity is said equivalent to 0.222 toe (apart from situations where the mass of fossil fuels consumed is given directly in toe units). For renewables, as they cannot be referred directly to heat, conventionally, they are referred to their potential calorific energy when used (final energy) so that 1MWh of renewable electricity (non thermal) is said equivalent to 0.086 toe, 3 times less than nuclear power. With these conventions, the total primary energy is 248.2 Mtoe, of which 119.2 Mtoe direct heat (with 101.86 fossil) and 129 Mtoe electricity (of which 7.3 Mtoe fossil).

These conventions, which were established to quantify the primary energy of nuclear and non thermal renewable electricity are frequently questioned; they do not put forward the advantages of a source, nuclear power, that does not emit carbon dioxide. If the same conversion rule based on final energy consumption were applied to all sources other than fossils, i.e. to all carbon free sources, the primary energy total of 248.2 Mtoe quoted above would now be 184.4 Mtoe[17].

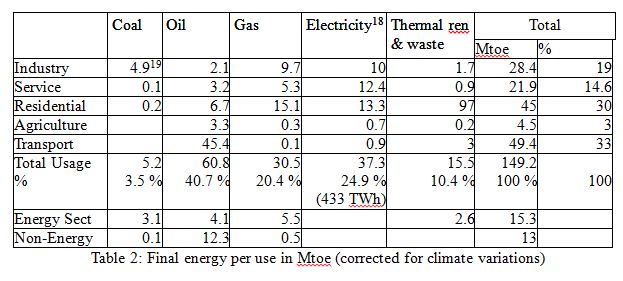

A 2) 2015 Final Energy Consumption per Usage in Mtoe

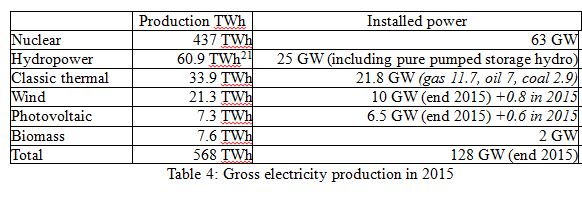

A 3) Specific Point on Electricity in 2015 (TWh)

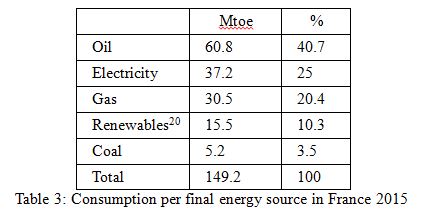

The 37.2 Mtoe for electricity stated in Table 3, final energy appraisal for 2015, correspond to 433 TWh (37.3 x 11.63) electricity at the end of the line on the distribution grid.

Tracing back to the gross production of 568 TWh (at the output of the production plants) includes the self consumption of the production units: 30 TWh, the export-import balance: 62 TWh, the pumped storage consumption: 8 TWh for 6 TWh produced, and line losses: about 35 TWh (roughly 7% of the energy transported).

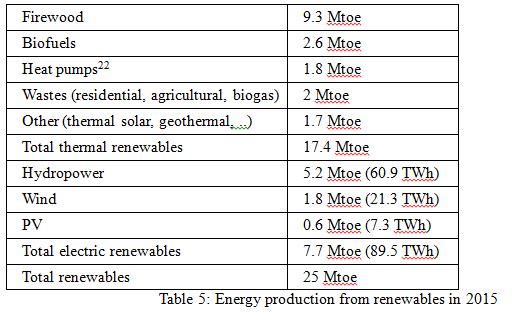

A 4) Specific Point on Renewable Energies in 2015

Fossil energies, a source of carbon dioxide emissions, account for almost half (46%) of the total primary energy sources and about 2/3 (65%) of direct use final energy, rising to 66% when the share of fossil energies consumed by the energy sector is included.

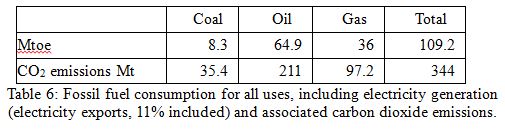

The carbon dioxide emissions due to these energies are given in the table below, along with the 2015 demand for these fuels. The emissions equivalence used is (cf. the preliminary remarks in the Introduction):

- Coal: 1 toe yields 1.17 tC

- Oil: 1 toe yields 0.89 tC

- Natural gas: 1 toe yields 0.74 tC

The conversion from tonnes of carbon, tC to tonnes of carbon dioxide, tCO2 is obtained by multiplying these values by 44/12=3.65.

Note:

Of the 344 million tonnes CO2 emitted, only 41 Mt are due to electricity generation. These emissions would be increased by 434 Mt, i.e. more than doubled, to reach a total of 778 Mt if nuclear power were to be replaced by a fifty-fifty mix of coal and gas; a remarkable result of the energy transition effected in the 1980s and 1990s.

To obtain the global CO2 emissions of France, we have to add the non energy related uses of 13 Mtoe fossils (see in Table 2) which would emit 41 Mt CO2.

B ) The Negatoe Approach: Beyond the Accomplished Coal Phase-Out

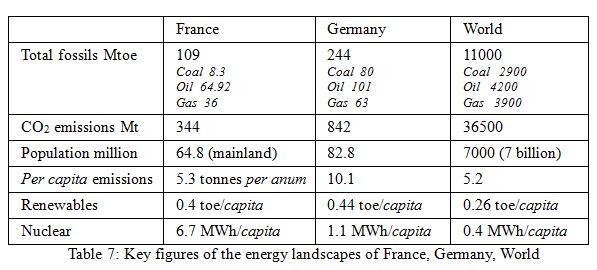

As shown in Table 7, France stands out from Germany, so close geographically, so similar in its standard of living and the per capita GDP, yet so different in the relative shares of coal, nuclear, renewables.

This particular situation of France (not unique, it is true also, for example, of Switzerland or of Sweden where nuclear and hydro power coexist) is the result of the energy transition in the years 1980-1990 in response to the oil crises. The transition led to the phasing out of coal and heavy oil and their replacement with nuclear power in the production of electricity so that the per capita[23] carbon dioxide emissions of France for energy production[24] as a whole are about 50% lower than those of Germany[25].

Note the close similarity of the German energy landscape with that of the rest of the world regarding the shares of the various components of the energy mix. Admittedly, the per capita emissions of France are somewhat larger than the world average; but, like the Chinese emissions, they tend to draw closer to it. In spite of this, at the European level and with a lack of subtlety, the same effort, namely the factor 4, is required of each member of the Union. If a factor 4 is applied to France, the factor for Germany should be on the order of 7.5, assuming constant population; in the event of an expected decline of the German population and growth of that of France, the factor for Germany should be even larger.

A successful first step towards fossil phase-out has been taken in France and an initial direction has been identified. The Negatoe scenario proposes to continue along the same lines, not for the sake of principles, nor because of rigidity or obstinateness, but because this route proves to offer the best energy security and least cost for households and for public finances, as well as the best competitiveness for businesses. Thus, Negatoe proposes to replace a large chunk of the oil and gas consumed for transportation and in building services with carbon free electricity produced at the least cost possible.

C ) An Outlook on the Future

In semi continuity, a reference, "Business as Usual" (B.A.U.)

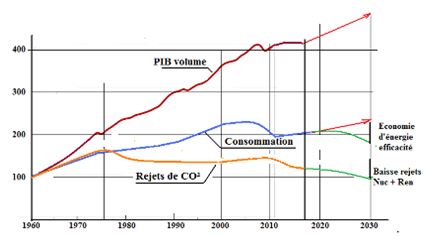

Looking back on the past it is possible to attempt an outlook on the future, barring fundamental changes, whether these are voluntary or not. Figure 1 shows how the significant parameters that determine the energy landscape and carbon dioxide emissions have evolved in the recent past, starting from a 100 index for 1960, and, anticipating on their future evolution, shows the direction in the Negatoe approach.

Figure 1 - Evolution of the GDP, energy consumption and carbon dioxide emissions for France; base 100 in 1960

By choosing 1960 as the starting date, the middle of the 30-year post-war boom, we highlight the effects of the oil and financial crises on the energy landscape.

Note, in the figure, the correlation of the evolution of the GDP with that of energy consumption, one following the other with more or less elasticity according to energy efficiency improvements. This efficiency improvement (ratio of the energy consumption growth rate to the GDP growth rate) was clear after the oil crises and the consequence of the indexing of energy costs to those of oil[26]. It dropped from about 0.75 to 0.63.

Figure 1 is very informative regarding the evolution of CO2 emissions. We note that they increase constantly up to the late 1970s, in parallel with increasing consumption and, beginning in the 1980s, they start to decline. This reversal is the consequence of nuclear power plants being brought into operation between the end of the 1970s and the end of the 1990s (from Fessenheim 1 in 1977 to Civaux 2 in 2000). It is also related to the increasing share of electricity in final energy consumption with, in particular, direct electric heating, in general associated to careful thermal isolation which is appreciated today[27]. This allowed a 15% reduction of CO2 emissions while final consumption increased by 25% between 1985 and 2009.

Nuclear power alone would account for 32% of the emissions gain. A first significant step, a guide if the overall objective for 2050 is to gain 75%.

Proceeding further, from now to 2050, in continuation with the objective of dividing carbon dioxide emissions by 4, implies making hypotheses on the evolution of the GDP and consumption.

The previous version of Negatoe referred to a "business as usual" type scenario (like the SR2008 scenario established by the DGEMP[28]) that hypothesized a 2.1%/yr growth of the GDP and a population of 70 million in 2050. This led to reaching 226 Mtoe final energy consumption in 2050 with 184 Mtoe in 2020, barring a radical change in the share of fossil energies, i.e. ignoring the factor 4 constraint. 184 Mtoe in 2020 meant a 23% increase with respect to the real situation in 2015 (149.2 Mtoe, see Table 2).

The financial crisis (early summer 2007) and the collapse of Lehman Brothers (September 2008) with the lasting effects that we still experience today, in particular in France, have completely disrupted the landscape with unforeseen changes in the GDP and energy consumption data. Indeed, while in 2007 the French GDP increased by 2.3%, it declined by 0.1% in 2008 and, more, by 3.1% in 2009. These drops are somewhat compensated, with difficulty, by a return to growth, +1.7% in 2010, +2% in 2011 but again, 0% in 2012 and a meager +0.3% to +0.4% from 2013 to 2016.

From the energy aspect, the extent of this crisis is visible on the primary energy evolution which, instead of increasing somewhat from the 276 Mtoe of 2006 declines to 260.1 Mtoe in 2015 (-5.7%). Similarly, final consumption drops from 161.7 Mtoe in 2006 to 149.2 Mtoe in 2015 (-7.7%). These declines do not result from voluntary energy consumption reductions but reflect a certain economic regression with its corollary unemployment and loss of purchasing power and their social consequences.

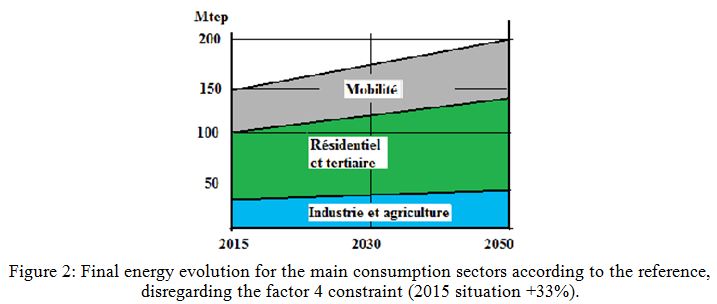

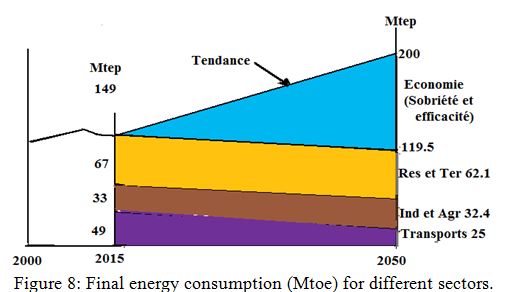

A more realistic 1.5%/yr GDP growth hypothesis from now to 2050 leads to a 70% GDP increase with respect to 2015. Assuming that the energy intensity, which is still improving, will vary from (about) 0.7 today to 0.5, the final energy consumption increase is 30%, leading to a 200 Mtoe final energy consumption in 2050. This could be the reference, in the absence of any specific supplementary actions taken to reach the factor 4, besides those already undertaken in the wake of the various crises we have known.

Figure 2: Final energy evolution for the main consumption sectors according to the reference, disregarding the factor 4 constraint (2015 situation +33%).

Continued fossil fuel consumption with the same trend is, obviously, incompatible with a factor 4 division of CO2 emissions. It's a long way to the factor 4; efforts will lead first to a stabilization of the emissions, before reducing them massively. Clearly, the longer we procrastinate, the more intense the effort will have to be. But actions must be undertaken in an orderly fashion; with spending directed to cheaper carbon emission reductions; taking into account investment payback and discount rate issues as well as potential technology improvements.

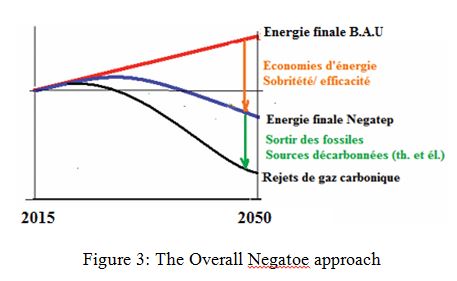

Overall, the reference scenario foresees significantly increased CO2 emissions, demonstrating the need to correct the consumption and energy production trajectories. Wherefore the Negatoe scenario approach, as illustrated in the figure below.

Figure 3: The Overall Negatoe approach

D) Energy Demand Management: 2050 Target

D.1 General Considerations

As already stated in the foreword, although reducing consumption is necessary to reach the factor 4, the real objective is carbon dioxide emission reduction and reducing consumption is only one of the means. Indeed, carbon dioxide emissions can well be significantly reduced while keeping final energy consumption constant.

Final energy needs have constantly increased (excepting a few short crisis related intervals, soon forgotten in the ensuing economic upswing), because of population increase and to the "forever more" per capita, as illustrated in Figure 1 for France. We hypothesize a population growth (for mainland France, from 64 million in 2015 to 72 million in 2050, i.e. +13%). In order to divide CO2 emissions by 4, if the substitution of fossil energies by carbon free sources is not sufficient, the per capita consumption will have to decline, in contradiction with past trends. This implies energy sobriety and efficiency.

- sobriety: individual wisdom that is satisfied with less, hopefully not enforced either directly by authoritarian measures or indirectly by financial constraints (to the point of being detrimental to health). Sobriety could, for example, lead to lower heating temperatures, smaller per capita residential surfaces (requiring less heating), more walking, more bicycle riding, using more public transportation, ... according to individual choices.

- efficiency: better satisfy the same needs by improving the yield of processes, in particular by recovering energy wastes ... Efficiency rests mostly on technology, creativity, industrial know-how. Housing insulation is one of its aspects.

The drive for better efficiency often comes with a significant cost, raising the issue of how to best allocate available resources. Keeping in mind that the purpose is to reduce CO2 emissions, measures should be selected according of their cost per tonne of avoided CO2. As a case in point and a quite actual one, should investments in renewable electricity production, such as wind turbines and solar photovoltaic panels be pursued, given that they do not significantly impact carbon dioxide emissions (or if they do, it is adversely), rather than investing in the insulation of buildings, including those heated with natural gas that could also switch to carbon-free electric heating in association with heat pumps where possible.

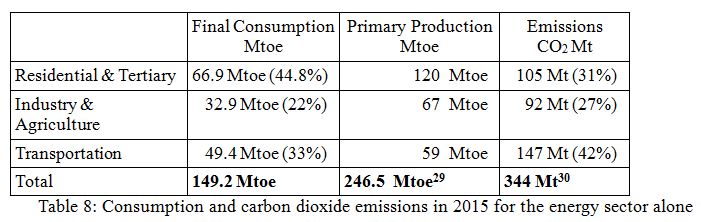

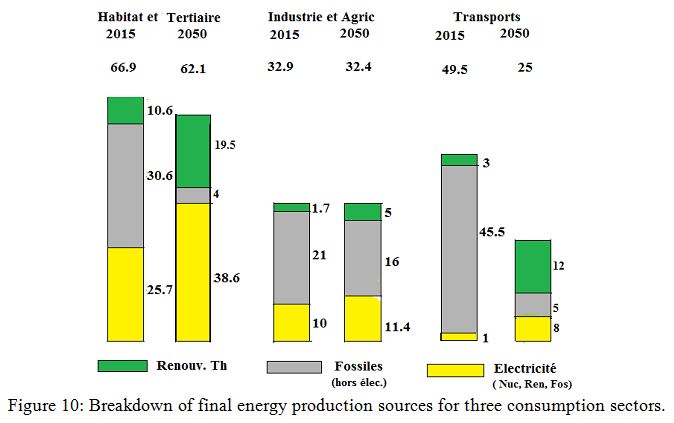

Qualitatively, the management of needs leads to monitoring the evolution of the data summarized in Table 8, i.e. consumption, production and emissions in the main occupational sectors in 2015. Note that these data do not necessarily evolve in parallel, they can even be opposed, one declining while another increases. Everything boils down to setting the number one objective and, in this instance, it is clear: reduce greenhouse gas emissions, in particular fossil fuel contributions.

The term efficiency mentioned above is explicitly stated in the very widely publicized European slogan "three 20 targets". In the European Union's climate-energy package adopted in 2008, one of the three 20s reads:

- To increase energy efficiency to save 20% of EU energy consumption by 2020.

The other targets are:

- To reduce emissions of greenhouse gases by 20% by 2020 taking 1990 emissions as the reference

and

- To reach 20% renewable energy in the total energy consumption in the EU by 2020.

For France, the three 20 targets are developed as:

- 20% reduction of greenhouse gas emissions

- 20% energy conservation by 2020

- 23% renewable energy in the final energy consumption mix[31]

Note:

While the EU text refers to efficiency, France mentions energy conservation. The two are quite different, efficiency being evaluated relative to the real GDP. If, for example, a country enjoys a 22.5% GDP increase over 15 years (+1.5%/yr) a 20% efficiency gain would translate, according to the EU phrasing, into a 2.5% energy consumption increase and, according to the French phrasing, a 20% reduction.

Unfortunately, in the setting of quantitative objectives in the form of the three 20s, a confusion is introduced between the objectives and the means. Merging the reduction of energy consumption with prescriptions on the share of renewables and greenhouse gas emissions reductions can lead to contradictory choices and environmental and economic nonsense. The same contradictions are there in the 2015 energy transition legislation as discussed above in the prologue. It is sometimes the case that a reduction of greenhouse gas emissions entails more primary energy (for example, electric heating from carbon free electricity or district heating with biomass compared to individual gas heating). Another example: replacing natural gas or oil fueled heating with firewood increases the final energy consumption but reduces CO2 emissions.

The Negatoe scenario introduces a hierarchy in the three 20 targets: there is only one target, the reduction of CO2 emissions and there are means, comprising decreased consumption and carbon free energy production. There is an additional objective: reduce CO2 emissions at least cost.

Since the Negatoe scenario does not retain CCS (Carbon Capture & Storage - see § F for the reasons) reducing CO2 emissions implies reducing the share of fossil fuels. After having phased-out coal and heavy oil (see § B), the consumption of gas must be reduced (essentially for heating) as that of oil (essentially for mobility and freight transport).

D 2: Residential Sector[32]

Responsible for 30% of the total final energy, the residential sector is the second energy consumption sector, just behind transportation (33%). However, with only 21% of the carbon dioxide emissions, it is far behind transportation (42% of total emissions). This is because of the relatively larger share of carbon free electricity (coal phase-out has already been accomplished) in the stationary residential uses (electric heating) and in industry as compared to mobility which relies practically 100% on oil, and where the transition remains to be done.

In mainland France, the 34.5 million dwellings comprise 28.4 million principal residences, 3.2 million secondary residences, and 2.8 million vacant dwellings. The number of occupied dwellings increases by about +1%/yr. In the reference scenario and in the Negatoe scenario, this value is retained. It is somewhat larger than the population increase, 0.4%/yr, (+8% by 2050). The mean residence area is 91m2. The per capita area was 35m2 in 1996, it is now 42m2 per capita[33]; this increase is expected to continue, whether in the reference scenario or in the Negatoe scenario, to reach 45m2 per capita: we do not consider restrictive measures such as decreeing apartment sharing[34].

Of the 34.5 million dwellings, 20 million were built before 1974, prior to the first legislation aimed at reducing energy consumption (consequence of the first major oil crisis). Another 9 million were built between 1975 and 1998[35] and 5 million were built since 1999. In recent years, about 300 000 new residences were built per year. With an average 50 000 per year residences torn down, the net increase is 250 000 per year or a 0.7% increase, larger than the 0.35%/yr population growth. In keeping with these tendencies, the total number of residential buildings in 2050 would be 43 million, the value retained also for Negatoe in 2050.

Insulation renovation work on residential buildings at the rate of 300 000 per year seems likely. Note that this renovation work can cover simple actions such as installing insulation in the attic all the way to the more complex total insulation[36]. Depending on the extent of the renovation work, a factor 2 to 4 improvement can be obtained[37].

In the reference scenario, the number of residences with reduced energy consumption, including new and renovated residences, would increase by 550 000 per year. Among the residences built before 1974, "heat sieves" or energy voracious residences would be eradicated[38].

Negatoe must proceed further, increasing the rate of new residential construction (400 000/yr) and of residence tearing down (150 000 per year) and, more important, the number of renovations: 400 000 per year; with better efficiency, to tend towards the factor 4 improvement mentioned above. Note that approximately 5 million residences require prompt action.

In 2015 the total final consumption in the residential sector was 45 Mtoe (522 TWh), distributed as follows: gas 32.1% (168 TWh); electricity 31.6% (165 TWh); oil 14.5% (76 TWh); firewood 15.5% (81 TWh); other 6.4% (wastes, LPG, coal)[39]. Today's average energy consumption, 190 kWh/m2.yr (17 500 kWh/yr per principal residence) would, in Negatoe, be reduced to lie between 100 and 50 by 2050 and sooner if possible. Heat represents about 62% of the energy needs in the sector, domestic hot water 12.1%, cooking 6.9% and specific electricity uses 18.9%, this last item increasing the fastest.

D 2.1: Heating

D 2.1.1 The situation today

- The consumption for heat amounts to 330 TWh (28 Mtoe). 50% of residences are heated with gas[40], 23% with electricity (direct heat, heat pumps excluded), 4% with district heating, 8% with firewood[41], 3% with heat pumps.

- 1.6 million residences are not equipped with heating devices, or only with summary means (cooking stove, independent devices such as mobile backup electric radiators, or - mostly open - fireplaces).

- The average consumption for heating is variable:

- For recent apartment buildings (year 2000) about 5 000 kWh/yr up to 8 000 kWh/yr for older buildings (1975 and earlier)[42]

- For recent individual houses (year 2000) about 11 000 kWh/yr, up to 25 000 kWh/yr for older ones (1975 and earlier).

D 2.1.2. What Does the Future Hold - Sobriety?

According to the legislation (of which the 1979 decree touting the abolition of wastefulness "chasse au gaspi") the interior temperature of dwellings should be kept at 19°C or below. This is not put in practice and mean temperatures of 21°C or even 22°C are frequent. Given that each additional degree represents a 7% consumption increase, it is tempting to decide that calling on civic mindedness, good will, education and a little enforcement, our consumption could be reduced by 15 to 20%. Clearly, the 19°C regulatory temperature does not coincide with the desired comfort zone of the majority[43]. This can only get worse with population aging. Only a significant energy price increase could, in the coming years, induce a reduction beyond 10%, and that would be for lack of funds.

D 2.1.3. Thermal Insulation of Dwellings and Renovation

Preliminary Comment:the flaws of the RT2012[44] that should be corrected urgently

Among other things, the thermal regulation sets, rightly, a limit to the energy consumption of buildings. Initiated in 1974, it has been constantly stepped up in its successive versions (1988, 2000, 2005 and finally 2012). Initially based on the final energy consumption in kWh/m2.yr (pointing directly and unambiguously to the dwelling's thermal losses and the quality of its insulation, tangible for the user who can monitor his kWh or, for gas, m3 consumption on his utility bills), from 2000 on, they were based on the primary energy consumption (a notion that is not directly accessible to the consumer), i.e. no longer on the quality of the dwelling itself but on the heating mode chosen. Electricity is then disadvantaged by a factor of about 2.6 and thus condemned indirectly while this heating mode is, in France, responsible for minimal carbon dioxide emissions since the electricity is produced essentially from nuclear and hydro power. The new RTs up to 2005 adapted this shift to primary energy by indirectly taking into account the effect of carbon dioxide emissions: two different primary energy limits were established according to the heating mode, with or without electricity. But this last item was completely deleted in the RT2012[45], disregarding the priority specified by the "Grenelle de l'Environnement[46]": limit carbon dioxide emissions. This new RT2012 does not include a limit on CO2 emissions, contrary to the recommendation of organizations such as the OPECST[47]. Unambiguously, the RT2012 fosters natural gas heating, thus inducing a carbon dioxide emissions increase.

Should the RT2012 be declared illegal?

Irrespective of the cost aspects which fall under the responsibility of the consumer, State legislation should impose only one criterion: the annual carbon dioxide emissions in kg per m2.

Since most of the electricity would be carbon free, Negatoe retains, for all needs (heating and other needs) the 50 kWh/m2.yr for new constructions and 100 kWh/m2.yr for older dwellings, as measured in final energy (not primary energy), as in the first few RTs.

- a) Heating, New Housing

The RT2012 thermal regulation requires 50 kWh/m2.yr primary energy on average in new housing[48]. While previous regulations took into account the low carbon dioxide emissions of electricity, RT 2012 makes no exception for dwellings heated by electricity (directly or with heat pumps). Note that this primary energy limit includes not just heating but also lighting, domestic hot water, and any auxiliaries (pumps and fans) via a "Cepmax[49]" coefficient. If, for electric heating, this limit requires heat pumps with a mandatory investment that represents no emissions gain, it is quasi unattainable for gas heated dwellings if the limits on carbon dioxide emissions are taken into account[50]. With a mere medium sized carbon tax, gas heating would be practically eliminated.

Given this situation, Negatoe retains a 50 kWh/m2.yr final energy consumption (not primary energy). This is the consumption today of well isolated, electrically heated, recently built housing. For the 14 million new constructions from now to 2050, this comes to 65 TWh, the value retained in Negatoe, in continuity with current new building construction.

- b) Heating in Older Housing & Renovation

An analytical approach is difficult given the variety of situations, building standards having evolved significantly, in particular in 1988 and 2005. The J. Orselli[51] report differentiates older housing (built before 1975), housing built between 1975 and 1995, and housing built since 1995. He takes into account older housing that has been torn down (a few %) and distinguishes two categories.

- Approximately 1/3 of older dwellings (nearly 6.7 million) are heated with electricity; they are generally well insulated (7MWh/yr final energy per dwelling or a total of 45TWh/yr).

- The other 2/3 are heated with other energy sources (about 20MWh/yr final energy per dwelling, or a total of 335 TWh/yr). These 335 TWh/yr include 95 TWh/yr (8.2 Mtoe) renewable energy (essentially rather inefficient wood-burning[52]) and 240 TWh/yr (20.5 Mtoe) fossil fuels.

In order to scale these 240 TWh (20.5 Mtoe) of fossil fuels down to 35 TWh (3 Mtoe) J. Orselli considers two scenarios and suggests a third one.

- One where renovation work is done at one go, aiming to reach very high quality insulation (opaque walls, double flow ventilation, well insulated glazing,...), drawing on the technology developed for new housing.

- One with so-called "diffuse renovation" that takes advantage of regular maintenance work to improve insulation by using good materials and techniques (windows, window and door frames, modern furnaces, ...)

- The third that combines diffuse renovation with a larger share of renewable energies and electric heating (but the report does not specify the conditions).

The first option runs the risk of very high costs, above 30 000 €[53] per dwelling[54], to reduce fossil consumption by only 3/4, scaling it down to 5MWh/yr per dwelling (a total of 60 TWh). To reach the 35 TWh/yr target, renewable energies or electricity should participate as a complement; we admit 2/3 renewable and 1/3 electricity.

With the second option, the fossil fuel heating needs for existing housing could be reduced by 50%[55], scaling them down to 10 MWh/yr on average (about 120 TWh total); the extra charge over and above the regular maintenance work would be small (on the order of 10 000 €) and easily compensated thanks to smaller fuel bills (and CO2 bills in the event of a real carbon tax). On the other hand, this option requires a significant increase of carbon free energy.

This comparison of the costs in the two scenarios is a perfect illustration of the decreasing efficiency rule: a 10 000 € investment reduces the demand from 20 to 10 MWh/yr per dwelling (useful energy) while a 30 000 € investment is needed to reduce it from 20 to 5 MWh/yr. So in some situations, depending on the final target, the investment to save one MWh may be close to 3 times as large, and the marginal investment to scale down from 10 to 5 MWh/yr may be 6 times as large[56].

The third option leaves things quite open. One possibility could be to supplement diffuse renovations with the addition of direct electric heating that is switched off during peak hours (peak shaving), the existing furnace taking over (a sort of hybrid heating system). This would significantly reduce fossil fuel consumption (by nearly 90%) while keeping existing furnaces in place[57]. Another possibility would be to combine diffuse renovation with renewable energy input in association with heat pumps, a solution that is likely to be more expensive but would offer greater flexibility to adapt to various situations. This is the path that Negatoe follows, proposing medium scale renovation to scale the final energy demand down from 200 to 100 kWh/m2, thanks to a 15 000 €/dwelling[58] investment (see § G for the total cost). Based on 400 000 renovations per year, i.e. a total 20 million dwellings renovated by 2050, the energy consumed to heat these renovated dwellings would be 182 TWh (instead of 380 TWh today).

Note: the Negatoe approach takes the Jevons paradox into account[59]

As previously stated, no specific action other than standard maintenance is considered for dwellings that are already well insulated, mostly electrically heated, and conform to the regulations prior to the RT 2012 (new constructions), i.e. 45 TWh. The heating total for dwellings, then, is 290 TWh, from which the energy relative to "fatal" sources such as cooking and a fraction of the specific usages (lighting, multimedia, ...) can be removed. We retain a total of 270 TWh (23.2 Mtoe) for heating, but point out that if it relied widely on heat pumps (see § D.2.1.4), the share of electricity would be 100 TWh.

D 2.1.4. Heating Energy Sources in the Residential Sector

To maximize the phasing out of gas and oil we are led to promote

- heat pumps (ideal for new constructions but also valid for renovations, including air source heat pumps)

- direct electric heating, already in use in new buildings

- hybrid 'peak shaving' electric heating as a complement to an existing oil or gas heating system where the fossil fuels (which can be stored) are used only during the limited peak demand periods

- biomass, assuming the quasi complete replacement of existing hearths with for instance: heavy large volume efficient wood burning stoves, wood pellet stoves. The large scale use of biomass to produce heat is dedicated as the base fuel for heat networks. Should individual firewood heating become widespread, particle filters are to be recommended; they are already installed in collective heating boiler rooms equipped with new biomass furnaces.

Note that little is expected from solar heating, as opposed to strong expectations for domestic hot water production (see § D.2.2). While domestic hot water is used all year round, solar heating for a dwelling would bring only little heat in the time of year when it is most needed and a lot when it is not needed at all, thus providing mediocre investment payback.

D 2.2: Domestic Hot Water

In 2015, the demand for domestic hot water amounted to about 59 TWh (an average of 2050 kWh per dwelling) with 27 TWh (46%) from electricity, 23 TWh (39%) from gas, 5 TWh (9%) from oil. The trend is an increasing per capita demand (+1%/yr) to which a +13% expected population increase by 2050 should be added. Proceeding from an awareness campaign where showers are promoted rather than baths and water flow management is encouraged, we posit that only the population growth will increase the demand, reaching 66 TWh in 2050. Energy sobriety cannot be enforced at the expense of health and good hygiene.

The transition away from gas and oil will occur thanks to solar thermal energy (solar water heating), heat pumps and also existing hot water tanks which, because they operate in low electricity demand periods, are compatible with a global view of "intelligent" and flexible electricity management[60].

D 2.3. Cooking

In existing housing, cooking represents about 34 TWh (15 TWh electric and 19 TWh gas) or about 1 200 kWh per dwelling. Assuming an evolution in parallel with the population, it will amount to 38 TWh in 2050, mostly electric.

D 2.4. Specific Electricity Uses

The demand for specific electricity uses amounted to 93 TWh in 2015, representing an average 3300 kWh per dwelling (including only principal residences)[61]. This amount results from a 150% increase over 20 years due to the basic equipment of households with "white products" (household electrical appliances: freezer, clothes dryer, dishwasher, microwave oven, ...) with an acceleration to reach +10 % per year in recent years. Add to this "brown products" (audiovisual media: TV, DVD player, console, Hi-Fi system, decoder, ...) and "gray products" (computer, printer, Wi-Fi, ...). Globally, the efficiency improvement of individual appliances, tending towards A+ grading, does not compensate for the increased number of appliances, nor for their increasing use. For 2050, we consider that, thanks to technological progress (better efficiency), there will be no increase due to the population growth and the diversity of usages. We keep the demand at 93 TWh.

Note:

Whenever an attempt is made at conserving electricity in its specific uses, one must make sure that, in return, the heating needs are not augmented; in the first analysis, one can consider that a significant part of specific electricity uses generates heat. This holds for all the appliances during the heating season and, in particular, for lighting.[62]

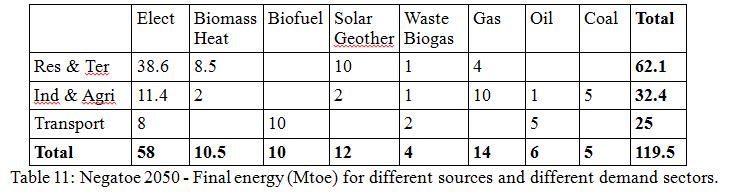

Recap: Residential Sector Demand 467 TWh (40.2 Mtoe)

This 467 TWh final energy consumption in 2050 is to be compared to the 695 TWh (522 x 1.33) of the reference scenario (a 48% global saving, that translates into a 66% saving per capita).

Comments:

- The Negatoe choice concerning energy efficiency (about 100 kWh/m2 final energy for renovation and 50 kWh/m2 for new constructions) does not necessarily lead to the least expensive solutions, considering today's price for the different energy sources. Various studies, in particular by Henri Prévot[63], show that an even more marked reliance on electricity would turn out less expensive. In Negatoe, we have chosen a balanced approach between energy efficiency and thermal renewables, for its better long term robustness.

- Similarly, the UFE - Union Française de l'Electricité (trade association for the French electricity sector) has examined the payback ratio of various energy efficiency solutions; they vary widely; UFE recommends that priorities be set keeping in mind that an investment with better payback will carry with it the possibility of later financing a less profitable, but useful investment[64].

D 3. Tertiary Sector

Office space, stores, education, administration, health, social action, sports, ... for a 1 000 million m2 total area (about 1/3 of the residential surface).

Existing equipment divide up as 50% gas, 23% electricity, 20% oil, 2% biomass, 4% networks. The final energy consumption in 2015 amounts to 254 TWh (21.9 Mtoe)

Heating and hot water production, technically comparable to those of the residential sector, account for a little more than half the above demand, the rest being consumed in specific electricity uses, similar to those of the residential sector. Electricity, then, represents 45% of the final consumption and gas 33% (mostly for heating with 46% of the surfaces).

The reference scenario foresees about 29 Mtoe (338 TWh) in 2050. The Orseli[65] report notes the large diversity of situations in the tertiary sector but considers several paths for its energy management, in particular:

- Apply the best technologies available in renovations and for new buildings, as in the residential sector (base 50 and 100 kWh/m2.yr).

- Manage intermittent occupation of many premises (offices, schools and sports equipment, stores, ...)

Air conditioning should increase in this sector more than in the residential sector but this trend cannot be really evaluated.

Given these qualitative elements, we consider that in this sector as in the residential sector, and contrary to the reference scenario which anticipates a 33% increase of the demand in the tertiary sector, the demand in the tertiary sector could decline by 10% total, i.e. 20% per capita, relative to the situation today.

The Negatoe objective to reduce fossil fuel consumption translates here into total oil phase out and the quasi total elimination of gas, both being replaced by thermal renewable energies for half the share and electricity for the other half, either using direct electric heat or via heat pumps. The connection of large tertiary facilities to heat networks should be actively promoted.

Recap: Tertiary Sector Demand - 254 TWh (21.9 Mtoe)

D 4. Industrial and Agricultural Sectors

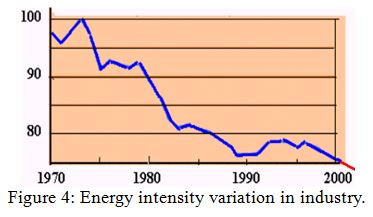

In 2015, the industrial and agri-food sectors consumed 32.9 Mtoe (382 TWh) with 28.4 Mtoe (330 TWh) for industry (including 4.7 for steel industry and 4.5 for agriculture. Industry consumed 38 Mtoe in 2002 and 37 in 2006. This sector was the most severely impacted by the economic crisis, with a decline to 28.4 Mtoe in 2015, as already mentioned. This decline is not due to improved energy efficiency, contrary to the decline of the 1980s, it is a direct consequence of the financial and economic crisis and of continuing de-industrialization that had already begun before the crisis. Industry had already worked hard at improving its energy efficiency after the oil crisis of the 1970s as shown in Figure 4[66].

Note, in particular, the development of variable speed motors[67], of recovery exchangers[68], ...

Figure 4: Energy intensity variation in industry.

While the trend would result in 38 Mtoe in 2050 for industry, can we still hope for efficiency gains?

These would be limited, as the improvements that were most accessible both financially and technically have already been implemented between 1975 and 1990, with a 25% gain over 15 years. We arbitrarily posit a 10% energy efficiency improvement between now and 2050. However, considering further industrial development likely[69], advantaged by the availability of competitive electricity thanks to nuclear power, the more so if oil prices return to higher levels, the total Negatoe consumption for industry in 2050 is kept at its 2015 level, i.e. 28.4 Mtoe. Large industrial energy consumers will probably rely increasingly on electricity, even for the elaboration of raw materials. This tendency will be reinforced as the price of fossil energies increases. The share of renewable energies should also increase (in particular in agriculture where biodiesel could partially replace heavy oil); it could reach 10%.

For agriculture, considering moderate efficiency improvements, we set the consumption at 4 Mtoe for Negatoe in 2050.

The resulting total for the industrial and agricultural sectors is 32.4 Mtoe in 2050.

Note: we should add to this total the needs that could arise from the biofuel industry, which is discussed in § D 5 (self consumption by the industry in the biofuel manufacturing process).

D 5 Transportation

Transportation today relies almost exclusively on oil. While it accounts for 33% of the final energy demand, it is responsible for 42% of the carbon dioxide emissions. No replacement energy sources are available today, nor in the near future at a large scale. Nevertheless, significant technological progress has allowed striking efficiency improvements in car combustion engines. A 2003 new car model emits 20g/km less CO2 than the 1995 model (12% gain)[70]. Up to the 2008 economic crisis, however, this improvement has been more than counterbalanced by stricter safety and anti-pollution legislation for substances other than CO2; by a consumer preference for more powerful vehicles; by more automobile traffic. The 2008 oil crisis has had a stronger psychological impact in the United States than in Europe. In France, it is the financial and economic crisis that has had consequences, with a scaling down of freight transport, but only slower growth, or quasi stabilization, of passenger transport. Governmental action in favor of low CO2 emitting cars (bonus-malus) has contributed significantly to reversing the trend.

D 5.1. Initial Conditions and Trend

In 2015, freight and passenger transportation can be characterized by:

- 323 Gtkm (Billion freight tonne-kilometers)

- Road 281; Rail 25; Waterway 8

with a significant crisis related reduction (-11% with 363 Gtkm in 2005)

- 928 Gpkm (Billion passenger-kilometers)

- Private vehicles 738; buses & coaches 71; rail 104; air 14 (domestic flights).

The rate of increase is small but has been continuous over 10 years (876 in 2005, i.e. +6%). The financial and economic crisis has had little impact, high oil prices having already been well incorporated in behavior.

The final energy consumption total is 49.2 Mtoe. Individual cars account for 25 Mtoe (with on average a little less than 2 passengers per vehicle for all types of car travel[71]), freight accounts for 17 Mtoe (trucks and light utility vehicles on roads 15 Mtoe; rail 1.4 Mtoe; waterways 0.4 Mtoe), air for 7 Mtoe (with 3/4 international flights including French overseas territories and 1/4 domestic flights).

The reference scenario would total 65 Mtoe in 2050.

D 5.2 Future: Sobriety and Efficiency

Compared to the present situation:

- technological progress should continue and become more general, with further reduced fuel consumption per km traveled and per tonne conveyed [72]. The fuel used per unit distance could decrease by 30% to 40% by 2050, with more emphasis on cars than on trucking.

- one can hope for a switch from cars to public transportation, modified behavior (ride-sharing, new city travel modes, ...) that could balance the population increase in terms of kilometers traveled.

- the transfer of freight transport from road to rail and waterways will be limited. Only a small fraction (about 30%) that covers medium sized distances (more than 500 km) could undergo a modal shift to rail or waterways. But beyond the difficulties relative to a necessary rail network extension, given that passenger rail transportation has priority, we place little hope in a large increase of the share of modal shift for freight; a shift to rail implies bulk breaking, making it less competitive.

- air transport demand for domestic flights could decrease by 50% but should not change much for overseas flights, if it does not increase (because of the population growth and a larger share of leisure travel).

On the other hand, while these theoretical gains would result in a 32 Mtoe demand, delays, systems inertia and the Jevons paradox (rebound effect) must be taken into account. Negatoe retains a 70% effective success rate, leading to a 35 Mtoe demand in 2050 based on the same share of fossil fuels as today. This is 29% less than today but 37% less per capita. The resulting energy management effort relative to 2015 is considerable (roughly -1%/yr). It is even more considerable relative to the reference scenario (almost a factor two).

D 5.3. Replacing Oil: Biofuels and Electricity

As discussed above, the demand can be cut back but the present allocation of resources has to be drastically revised, with a radical reduction of the share of oil if strong action on carbon dioxide is to be undertaken[73]. A revolution is necessary and the quasi total domination of oil abandoned, with a shift to biofuels and electricity provided the latter is carbon free. Clearly, though, this revolution will take place in a context where the efficiency improvement of combustion engines competes and is complementary with the shift.

Oil could be replaced with synthetic fuels produced from coal (CTL) or gas (GTL). In the absence of massive CO2 capture and storage[74], these options do not fundamentally change the picture vis-à- vis the greenhouse effect and reaching the factor 4 (it would be even worse with CTL).

D 5.3.1 Biofuels

A 2003 European directive had set a 5.75% (LHV) biofuels target in 2010 which translates, for France to 2.8 Mtoe. This is practically reached with 2.6 Mtoe in 2015, based on the present so-called first generation technology and standard European agriculture, with the processing of beets, wheat, rape ... But this production requires external energy input and, considering the energy (fossil so far) consumed to produce the biofuels, the real net value is much less and can be estimated to be 1.5 Mtoe. Proceeding much further seems problematic. Raw materials would have to be imported[75]; agricultural resources are limited and mobility would rapidly be competing with food supply. In net contribution, not including imports, the limit would lie between 3 and 5 Mtoe, far removed from the needs. Moreover, the net appraisal of greenhouse gas emissions is far from the one hoped for.

Fortunately, new potential production capacity is identified with lignocellulosic biomass (second generation biofuels), and production enhancement thanks to external energy input sources[76]. In self consumption with a close to 40% energy return, about 1.5 GJ energy has to be added to produce 1 GJ biofuel from 1 GJ biomass; this energy has to be carbon free, it can be either biomass (starting from 2.5 Mtoe biomass, 1 Mtoe biofuel could be produced and the self consumption covered) or it can be electricity, or again, a combination of the two, depending on the respective prices of biomass and electricity, and on biomass scarcity.

Note 1:

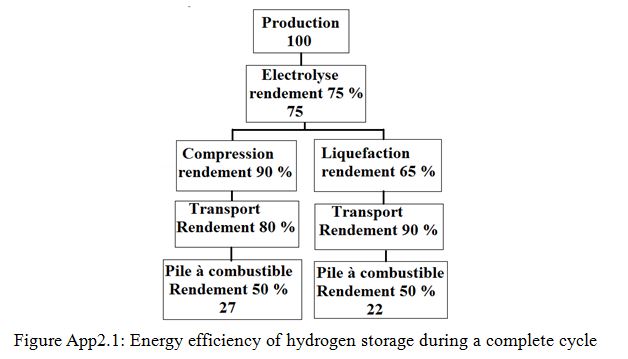

In theory, value can be added to the biomass with external hydrogen input. Indeed, the proportion of hydrogen relative to the carbon is smaller in the plant than in hydrocarbon. The plant composition is C6H9O4, i.e. a proportion of 3 hydrogen atoms for 2 carbon atoms; in hydrocarbon, the proportion is 2 hydrogen atoms for each carbon atom, or 4 hydrogen atoms for 2 carbon atoms. The plant's carbon can thus be put to better use with hydrogen feed in. The theoretical mass return can then reach 58% and, in practice, 40% to 50%. With 1 tonne raw material and hydrogen feed in, it would be possible to produce 0.4 tonne liquid biofuel with the same properties as today's fuels derived from oil. However hydrogen production takes energy so that altogether, the balance is not good, the global energy return is obviously poor (final energy return relative to factory entry 40% to 50%, primary energy return about 25%) and the investments larger (in addition to the biomass-to-liquid (BTL) investments, the hydrogen production investments). This approach could become attractive if biomass were to become very expensive. In that case, the process could be taken further with "hydrogen enrichment" (see Appendix 2, Electricity and Hydrogen).

Note 2:

Another possibility is to produce biogas fuels (biomethane) instead of liquid biofuels. The synthesis of methane from lignocellulosic biomass is achieved preferably via the thermodynamic process (see Appendix 3) used for liquid fuels. The return is better since the synthesis reaction is exothermic. However, when taking into account the necessary gas cleaning process to upgrade to methane, as well as the whole logistics to bring the gas to the filling station outlet, it is wise to retain a global return similar to that of liquid biofuel production (40% to 50%). The choice between liquid or gaseous fuels will then rest on usage convenience: liquid as a direct substitute for gasoline or diesel, or gas to power a fuel cell (FC for instance PEMFC). However, even if the hoped for technological progress is successful in developing an affordable methane fuel cell, pressurized methane will be required to provide an acceptable distance range.

Given these elements, in Negatoe for 2050, we retain 10 Mtoe liquid biofuels, measured as final energy (measurable by the user at the gas pump) produced from 17.5 Mtoe biomass and 7.5 Mtoe electricity (the necessary 15 Mtoe energy being provided equally by biomass self consumption and by electricity, here 87 TWh).

Note: 10 Mtoe biofuel could be produced with a different combination[77], for example: Biomass 7.2 Mtoe; Electricity 11.3 Mtoe; Gas 0.8 Mtoe.

Add to this 2 Mtoe methanation biogas (see Appendix 3), essentially for local transportation usage in agriculture and public utilities. Biogas can come to compete with liquid biofuels, but overall, both are based on the same limited amount of biomass.

D 5.3.2. Electricity

Besides biofuels, which will not be sufficient to come near the factor 4, a contribution from electricity is a possibility, provided it is not produced from fossil fuels. Electricity can be used directly, to power public transportation (trains, trams, subways,...) it can also extend to individual transportation, thanks to the development of batteries, for use in 100% electric vehicles or in rechargeable hybrids. Fully electric vehicles can cater to city or city and vicinity needs (typically the second car[78]). Rechargeable hybrid vehicles can do with smaller capacity batteries; with a 100 km range, for example, they should satisfy most of the daily journeys which do not cover more than 40 km on average, while consuming practically only electricity[79].

All told, with electric and hybrid vehicles, the equivalent of 15 Mtoe oil should be replaceable with 5 Mtoe electricity (58 TWh).

D 5.4. Transportation Recap

Starting from today's 49.2 Mtoe final energy consumption and counting on conservation amounting to 14 Mtoe (technology improvements, city organization, individual behavior) and, more than anything else, the leading role of electric transportation and its efficiency in terms of useful energy (3 times better than with combustion engines) we obtain 23 Mtoe final energy, a 53% gain relative to the 2015 situation and a 65% gain relative to the reference scenario.

This is achieved with the following distribution:

- electric public transportation 3 Mtoe[80] (35 TWh)

- electric or hybrid cars 5 Mtoe (replacing 15 Mtoe oil) (58 TWh*)

- liquid biofuels 10 Mtoe (produced from 17.5 Mtoe biomass

and 7.5 Mtoe electricity)

- biogas 2 Mtoe

- oil 5 Mtoe

Transportation is thoroughly disrupted, more so than any of the other sectors. This appears to be both feasible and reasonable, provided the transportation demand management efforts (technological progress, public transportation development, city planning,...) are successful. If only 9 Mtoe were saved instead of 14 Mtoe, the share of electricity would have to be increased by about 2 Mtoe (+23 TWh).

*Note: The 58 TWh correspond to battery charging.

As discussed in Appendix 1 (see the smart grid and demand spreading), the variations of the daily total power demand observed on the grid are on the order of 20 GW. The smooth distribution of charging hours(seeking mostly night hours, e.g. the car in the garage charging between 9 PM and 7 AM) should allow demand satisfaction without requiring additional installed power (obviously favorable for the nuclear load factor).[81]

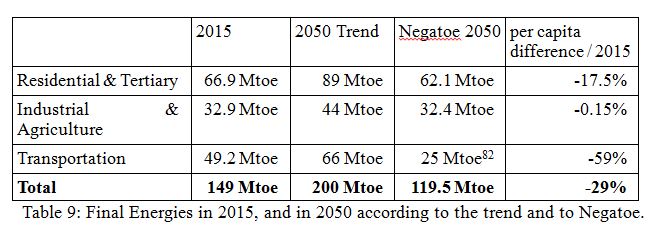

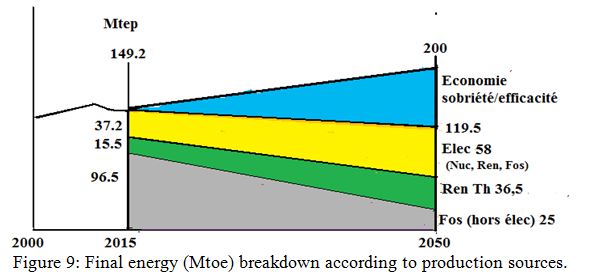

D 6 Global Recap: Final Energy Demand

Table 9: Final Energies in 2015, and in 2050 according to the trend and to Negatoe.

E) Carbon Free Energy Sources from Now to 2050

Reducing the share of fossil fuels implies, barring drastic energy conservation, calling on carbon free energy sources: renewables[83] and nuclear power. Today, in France, renewables provide 25.1 Mtoe primary energy (9.4% of the total) and nuclear power provides 114 Mtoe (43%), while fossil fuels ensure 109.3 Mtoe (44%). Reducing these by a factor close to 4, i.e. an 82 Mtoe reduction, cannot be achieved solely by energy conservation which, as discussed above, could amount to 29.5 Mtoe final energy relative to 2015 (149.2 - 119.5). In first approximation, the 52.5 Mtoe discrepancy (82 - 29.5) has to be filled with carbon free sources whether they generate direct heat, or heat and electricity from a single source (cogeneration), or only direct electricity.

E 1. Renewable Direct Heat Sources

E 1.1. Biomass, Biogas, Carbonaceous Wastes

Consisting of wood fuel from forests, various agricultural and household wastes, first generation biofuels, the resource today amounts to 13.9 Mtoe primary energy[84].

- a) Wood Fuel